In light of the future adoption of laws regulating blockchain technology and cryptocurrencies, including the Bill on Digital Assets (“Bill”), blockchain and smart contracts will soon enter the Serbian legislation.

Concept and meaning

Blockchain comes from the words “block” and “chain”. It is a way of performing transactions placed in blocks, the blocks being linked in a chain, so that it is not possible to change one block and leave the others unchanged. The blocks are interconnected and cryptographically locked. Blockchain is completely secure, transparent and anonymous.

Each new block has its own time stamp, corresponding to the data entry. A new block always contains the information about the old block.

The significance of the blockchain is reflected in the fact that the classic trust in a legal transaction is changed by checking the data in blocks. Blockchain is, actually, a kind of online book in which the data on executed transactions are recorded.

Legal regulation

Due to the insufficient development of blockchain in Serbia this concept is still relatively unknown to people.

According to the announcements from the Chamber of Commerce of Serbia, we could soon expect a Bill on Blockchain Technology and its application in cryptocurrency trading. It has been announced that blockchain technology would be applied when trading with electronic currencies (Bitcoin, Ripple, Libra, etc.). Trade in electronic currencies is still not regulated in Serbia which is why users mostly resort to foreign sites. However, having in mind how many programmers work in Serbia, a big increase in the use of this technology can be expected after the law comes into practice.

Also relevant for blockchain is the Bill on Digital Assets, published by the Ministry of Finance in mid-October 2020, which should regulate the acquisition of digital assets, cryptocurrency, smart contracts, and digital tokens.

The Bill introduces the term “mining”. Mining is the process of adding transaction records to a bitcoin public registry – blockchain.

Acquisition of digital assets by participating in providing computer verifications of transactions related to specific digital assets (mining of digital assets) is allowed, but the provisions of the Bill do not apply to the acquirers. Therefore, mining is allowed, but the Bill does not apply to the digital property acquired by mining.

However, digital assets acquired by mining may be traded by the holders of these assets either by using the services of service providers, in which case the provisions of the Bill are applicable to the users, or on the OTC market (digital asset trading market in which transactions are conducted directly between the seller and buyer of digital assets without service providers and outside digital asset trading platforms).

Many countries take seriously the problem of blockchain regulation. The United States is among the first, followed by France, Belarus, Japan, Portugal, and others.

Finally, it can be said that blockchain is one of the safest ways to perform electronic transactions. It would be much easier and cheaper for users to complete their legal affairs in this way.

With clear legal regulations, this technology could expand and largely replace the existing ways of concluding contracts.

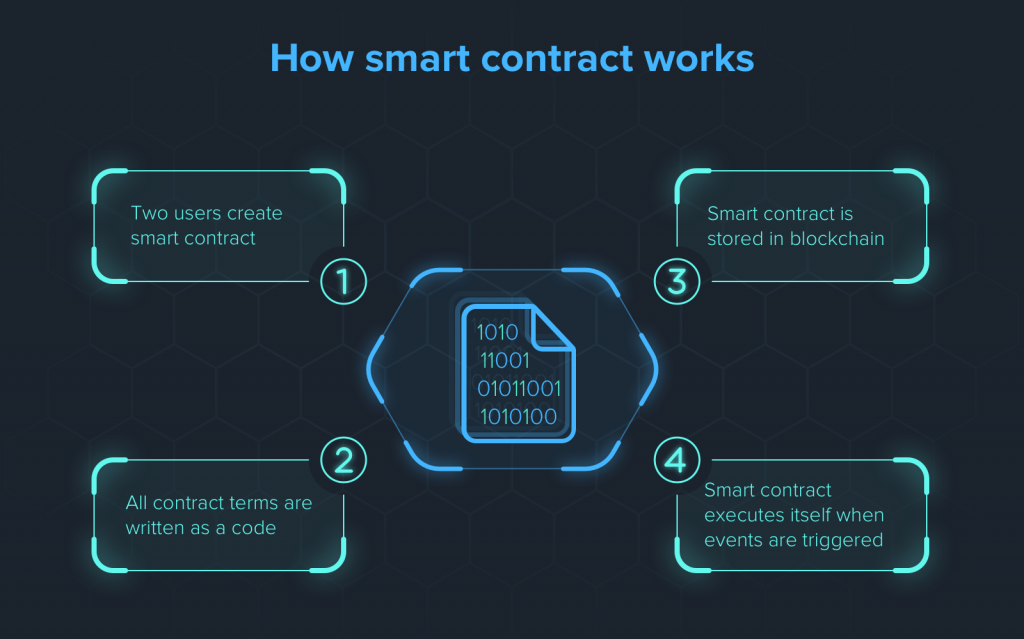

How does a smart contract work?

The most interesting thing about blockchain is its application. The concept of smart contracts has developed in the United States. When the appropriate assumptions determined by the program code are met, the contract is automatically executed. Therefore, in these contracts, the contractors do not have to think about whether the other contracting party will fulfil its obligation or not, because this is performed automatically. Smart contracts are based on blockchain because the data about those contracts is stored in blockchain. The data are distributed to the computer network and thus become immutable. A smart contract differs from an electronic contract because it is made in a programming language. Therefore, when the data are inserted into the chain, the code remains unchanged and self-executing.

Smart contracts connect people around the world who thus securely exchange goods and services at a slight cost, relying solely on the computer and its software.

The Bill particularly stipulates that the lien contract can be executed in the form of a smart contract, which the Bill defines as a computer program or protocol based on distributed database technology or similar technologies which in whole or in part automatically performs, controls or documents legally relevant actions or events in accordance with the already concluded contract. Interestingly enough, the Bill prescribes the principle of technological neutrality according to which the provisions of this Bill apply to all digital property regardless of the technology on which it is based. Therefore, in practice, the enforcement procedure could be significantly shortened and facilitated through automatic collection from the value of digital property if the debtor does not settle a due obligation.

Examples of smart contracts in everyday business

Online purchase – You have ordered goods through an online shop. Your payment is recorded in the blockchain. After the delivery service confirms the delivery, the money is transferred to the seller through the system.

Lease agreement – You have entered into a lease agreement. The contract stipulates the rent payment should be effected by the 10th of the month. In case the tenant does not pay the due rent, the blockchain system locks the door and the tenant can no longer enter the business premises. However, bear in mind that in case such action is not stipulated by the agreement (the landlord’s right to ban the entrance into a flat or building, etc.), the tenant could file a lawsuit for disturbance of possession, demanding the handover of the building, flat, etc.

Inheritance – You can testate your property by the Will or by entering into a Life Care Agreement using smart contracts. The system checks the existence of a death certificate for a certain person and automatically executes the Will or the Life Care Agreement, without an intermediary. The system sends the data to the cadastre so it can register the ownership, to the tax administration for paying taxes, and to all other necessary records.

Smart contract challenges

The issue of changing the established rights and obligations of the contracting parties, i.e. the annexation of an agreement, will happen by simply updating the software itself, thus resolving the issue of applying the institute of changed circumstances.

The crucial problem lies in the impossibility of a transaction not to be executed or revoked if the foreseen conditions are met. Basically, it is irreversible, and this fact will certainly make some serious troubles in terms of legal transactions based on blockchain.

Recent Comments